Stewarding Your Money

In part one of this essay we discussed what causes general price levels to rise, what the true definition of inflation is and how trustworthy government statistics are. We continue in part two with a brief look at some common misconceptions concerning modern banking and how chronic inflation can tear at the fabric of society. We close with summary observations for your consideration.

Note that South Middlesex Baptist Church is not a financial institution and is not insured by the FDIC. Any references to the Federal Deposit Insurance Corporation (FDIC), including its name or logo, are used solely for educational and illustrative purposes and do not imply endorsement or affiliation. The authors are not investment advisors and nothing in this article is to be taken as investment advice. Readers are encouraged to study the issues raised here for themselves and to take whatever steps they deem necessary to be good stewards of the worldly wealth God has entrusted to their care.

Myth 3: The Money In My Bank Account Is Actually There

Fractional reserve banking in the US has been carried to a dangerous extreme. Mandatory bank reserves in the US have been reduced to zero and banks only maintain enough cash on hand to pay a tiny fraction of potential withdrawals. People are conditioned to believe their money is sitting there in the bank, safe and sound, available to withdraw at any time. The fact is that most of it is not there at all. It has been loaned out or otherwise used by the bank for its own purposes. If too many depositors tried to withdraw their money at the same time, there would not be enough money in the banking system to pay them.

While the Federal Reserve Bank can and does inflate the money supply by creating new money out of thin air, commercial banks also lend new money into existence. New loans produce new bank deposits and new bank deposits produce more new loans. See the problem? The process feeds upon itself. In addition to that, new lines of credit are also inflationary. When a bank issues a new credit card with a spending limit of, say, $10,000, that instantly increases the dollars available for spending in the economy by a like amount.

The creation of money and credit, the real role and activities of the secretive Federal Reserve Bank and how the government actually funds its activities are intentionally complicated. We are not supposed to know how it all works! We are supposed to trust the system, pay our taxes and not ask too many questions.

Scripture speaks directly to this kind of dynamic, not in the language of modern finance, but in the language of truth, transparency and just stewardship. God repeatedly condemns systems that create the appearance of stability while hiding unseen instability. Through the prophet Jeremiah, God rebuked leaders who reassured the people with comforting illusions:

“They dress the wound of my people as though it were not serious, saying ‘Peace, peace,’ when there is no peace.” - Jeremiah 6:14

In other words, they told the people everything was fine when it wasn’t. They lied, offering false confidence instead of truth and illusion instead of integrity.

The promise of the banking system, that your money is safe and available, functions in much the same way. It creates a sense of security that does not match reality. And Scripture consistently warns against systems built on false balances, hidden risks and misleading assurances. God’s standard is simple:

“Provide things honest in the sight of all men.” - Romans 12:17

“The Lord detests dishonest scales.” - Proverbs 11:1

A system that tells people their money is available while simultaneously lending most of it to others is, in biblical terms, a dishonest scale. In modern terms, it is a fraud.

Myth 4: FDIC Deposit Insurance Is All We Need To Protect Our Bank Deposits

The Federal Deposit Insurance Corporation (FDIC) insures deposits against bank failure up to certain limits. Stickers on teller windows comfort depositors, assuring them that their money is safe and sound, even though the banks don’t actually have it. This has been called, “the sticker principle.” When you check FDIC reserves against insured deposits, however, you find that this government agency only has about one cent in reserve for every dollar of insured deposits.

That means it can handle a few isolated bank failures, but if a number of banks get into trouble at the same time, there isn’t enough money in the fund to pay depositors. We leave it to the reader to surmise how the government would solve that problem. Hint: More inflation is one of the easiest solutions. The FDIC name/logo is used here for illustrative purposes only; no affiliation or endorsement is implied.

Here again, Scripture speaks with remarkable clarity. The Bible has a category for promises that sound reassuring but lack the strength to deliver. God calls them false assurances, words that soothe the public while hiding the underlying problems.

Through the prophet Ezekiel, God described leaders who built walls of weak material and then covered them with whitewash to make them look strong:

“Because they lead my people astray, saying, ‘Peace,’ when there is no peace…they smear whitewash on flimsy walls.” - Ezekiel 13:10-12

The FDIC sticker functions much the same way. It is whitewash on a flimsy wall. It gives the appearance of strength, but the underlying structure is weak, vulnerable and dependent on the very mechanism - excessive money creation - that causes rising prices.

The problem is not that the FDIC exists. The problem is that people place their trust in a guarantee that cannot withstand systemic stress. It is a promise that only works as long as it is not truly needed. In other words, it is a confidence game run by con artists.

Myth 5: The Money In My Bank Account Belongs To Me

When you deposit money in your bank, you make what amounts to an unsecured loan. The money is no longer yours. What you still think of as your money becomes a bank asset. If the bank gets into trouble by making bad investments or bad loans with your money, you have what amounts to an IOU from the bank plus FDIC insurance with a reserve fund of 1/100th of insured deposits. That is all the protection you have. But it’s even worse than that.

In a banking crisis, bank regulations now allow for what is referred to as “bail-ins.” This is where depositors’ money is used to satisfy bank obligations. When the government rescues a bank with your tax money it is called a bail-out. When you personally rescue a bank against your will by having some of your deposits confiscated, it is called a bail-in. Think of a bail-in as a bankruptcy where the creditors only get some of their money back. The “bail-in” concept was first tested in Cyprus some years ago when that country experienced a banking crisis. The US now has laws that allow the same thing to happen here. Bank regulations also allow banks to limit withdrawals under certain conditions.

The Bible warns repeatedly against trusting in systems that promise stability but cannot deliver. Through the prophet Habakkuk, God condemned those who built their wealth on the backs of others through unjust structures:

“Woe to him who piles up stolen goods and makes himself wealthy by extortion!” - Habakkuk 2:6

Strictly speaking, a bail-in is not extortion, but the end result is the same. The losses of the institution are shifted to the people who trusted it. Bail-ins are nothing more than another form of theft whereby the system protects itself at the expense of the people it is supposed to serve.

The Bible also speaks about the illusion of ownership. Jesus told a parable about a man who believed his wealth was secure only to find that his confidence was misplaced:

“This is how it will be with whoever stores up things for themselves but is not rich toward God.” - Luke 12:21

The point is not that saving is wrong, but that false confidence in fragile systems is dangerous. The man in Jesus’ parable believed his wealth was safe because he had secured it in barns. Many today believe their wealth is safe because they have secured it in banks. But barns can burn and banks can fail. The issue is not the storage of wealth, it is misplaced trust.

From a biblical perspective, the idea that your bank deposits belong to you is at best a half-truth. Legally, the money belongs to the bank. Practically, it is at risk in a crisis. Spiritually, it is a reminder that earthly systems are fragile and that God calls His people to wisdom, discernment and a sober understanding of the world in which they live.

Myth 6: A Little Bit Of Inflation Is Good

The Federal Reserve Bank (“the Fed”) has a target inflation rate of 2% per year. Of course, actual inflation exceeds that rate by a large margin, but even if the Fed achieved its 2% goal, the purchasing power of the dollar would fall by roughly 20% in only ten years. In other words, after ten years of 2% inflation, it will take $100 to buy what $80 will buy today. Real life experience has been much worse.

Inflation does serious, fundamental damage to the fabric of society. In 1963, the average first-time homebuyer was 26 to 27 years old. Today the first-time homebuyer is closer to 40 years old. Among the drivers of this disturbing trend are later marriages and crushing student debt burdens. We assert that the root cause of both of those factors is inflation. The biggest thing making homes unaffordable, however, even more important than artificially low interest rates, is the fact that home costs have risen much faster than wages. This is also due to inflation of the money supply. Central bank (Federal Reserve) money printing always makes asset prices rise faster than incomes.

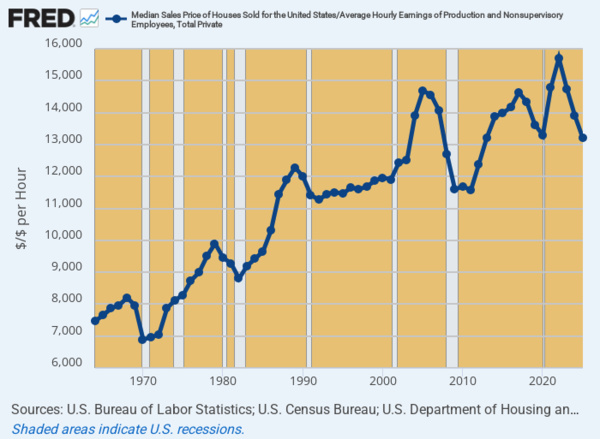

The accompanying chart shows how many hours a non-supervisory employee had to work to purchase a median value home over the years. This has risen from about 7,000 hours in 1970 to nearly 14,000 hours today. In other words, workers had to pay roughly three and one-third years of wages to buy a home in 1970. Today, workers have to pay almost seven years of wages to buy a home. Clearly, wages rose nowhere near as fast as home prices.

Not only can young people not afford to buy houses, they can’t afford to marry and have children, either. According to the Centers for Disease Control (CDC), U.S. birth rates just hit record lows. More babies were born in this country in 1966, when the population was only 196 million people, than were born during 2025, with a population of 343 million people. We live in a society that is struggling, largely due to inflation and the rising prices it causes. Young adults are marrying later, having fewer children, unable to save and are having a tough time buying a home. The biggest factor behind all of this societal damage is inflation, also known as money printing and currency debasement.

Final Thoughts

Many factors not mentioned here, such as temporary shortages, interest rate changes, supply disruptions and geopolitical instability can cause prices to rise. The main driver of general price level increases, however, since the early part of the last century has been inflation. Inflation is larceny on a grand scale. It is theft so cleverly disguised that most people don’t see what’s going on right under their noses. Essentially, inflation and fraudulent banking practices are violations of two of God’s most fundamental laws:

“Thou shalt not steal.” - Exodus 20:15

“Thou shalt not bear false witness…” - Exodus 20:16

If government officials and their partners in the banking industry obeyed those two commandments, we would have sound money and safe banking. Prices wouldn’t be rising or even remaining the same. They would be falling due to continuing advances in technology. Savers and pensioners would see their wealth increasing instead of melting away.

We have touched only briefly on six of many myths and misconceptions about inflation and banking in the U.S. There are many more myths and much more to be said about each of them. A strong case can be made that the financial system in much of the world, including the U.S., is a house of cards, a confidence game lacking real safeguards to protect average citizens in the event of a crisis. We encourage you, dear reader, to investigate these issues more deeply on your own. It is our sincere hope that your investigation, together with independent thought and subsequent action, will lead to greater financial security for you and those you love.

We also urge you to turn to Scripture and prayer for guidance. Scripture offers both realism and hope. Earthly systems are weak, but God is strong. Human institutions are unstable, but His kingdom is unshakable. Men lie, but God’s Word is truth. Financial institutions are built on shifting sands, but God’s wisdom is a rock beneath our feet. We close with these words from the book of Proverbs:

“The fear of the Lord is the beginning of wisdom.” - Proverbs 9:10